Revenue Recognition and Accounts Receivable-Part 2:

Boosting Sales Through Channel Stuffing

“I would gladly pay you Tuesday for a hamburger today.”

-Wimpy

In our last installment, we looked at how rising accounts receivable may be an indication that customers are not paying their bills. That is usually the first thing that most analysts associate with an unhealthy increase in days sales outstanding (DSOs). (See “Revenue Recognition and Accounts Receivable- Part 1” for a primer on DSOs). However, we believe the much more common and potentially damaging problem a rising DSO figure may be indicating is the inflation of current sales figures by pulling revenue into the current quarter through offering easier credit terms. This practice is sometimes referred to as “channel stuffing” and is the topic we will explore today.

Imagine a salesperson who is below her quota and December 31st is fast approaching. She knows several customers are thinking of placing orders early in January, so she calls them and tells them if they will buy in December, they will have 60 days to pay the bill instead of their normal 30-day payment term. This is enough to push several of them over the line, allowing the quota to be met. However, the celebration is short-lived as the salesperson was originally expecting to count those sales towards the upcoming March quarter. She now has three months to come up with new customers to take their place or she will miss her quota for the upcoming quarter.

This activity happens all the time at the company level which we frequently see signs of in the form of rising DSOs. We regularly see companies admit in financial filings that they have extended payments terms for customers for various reasons. Often, this allows sales growth to be boosted or maintained for a short while but the game of robbing the next quarter to make the current one usually ends badly and abruptly.

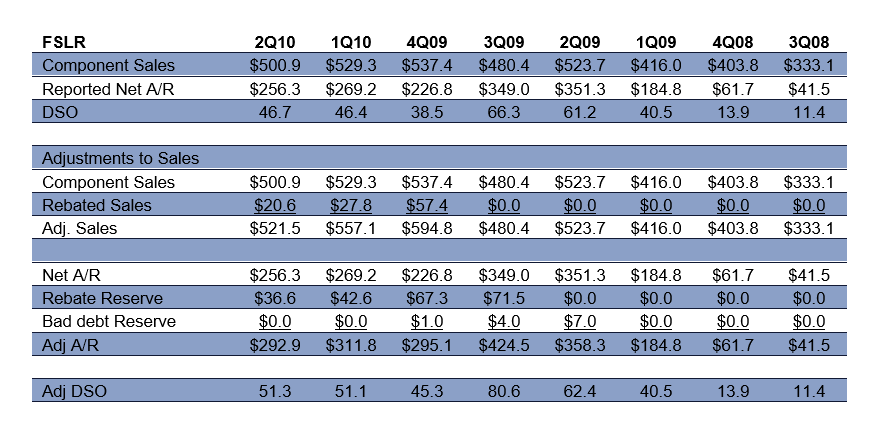

The Case of First Solar

We documented a rather dramatic example of easier credit terms boosting sales and DSOs in the results of First Solar, Inc. (FSLR) in the 2009-2010 timeframe. FSLR is a leading manufacturer of solar panels that was enjoying rapidly rising revenue. The following table shows the company’s sales, receivables, and DSOs from the third quarter of 2008 through the second quarter of 2010. We made several other adjustments to those numbers in the latter half of the table which we will explain as we go. For now, just focus on the top three lines. (Also note that we utilized component sales and did not include system sales as they were immaterial and more closely tied to unbilled receivables.)

Before 2009, FLSR’s payment terms allowed customers 10 days to pay their invoices. However, in the first quarter of 2009, the company amended those terms to allow customers up to 45 days to pay. We see in the above table that DSOs immediately turned upward, climbing from 11 days in 3Q08 to a peak of 66 by 3Q09. The company described this in the footnotes of its 10-Q filing for the first quarter of 2009:

“The increase in accounts receivable was mainly due to the amendment of certain customers' long-term supply contracts, that extended our customers’ payment terms from 10 days to 45 days, net as well as the timing of shipments to customers during the three months ended March 28, 2009.”

To slightly complicate the analysis, FSLR instituted a rebate program in the 3Q09 quarter which is explained in the following note found in the 10-Q:

“During the three months ended September 26, 2009, we amended our Long Term Supply Contracts with certain of our customers to implement a program which extends a price rebate to certain of these customers for solar modules purchased from us. The intent of this program is to enable our customers to successfully compete in our core segments in Germany. The rebate program applies a specified rebate rate to solar modules sold for solar power projects in Germany at the beginning of each quarter for the upcoming quarter. The rebate program is subject to periodic review and we will adjust the rebate rate quarterly upward or downward as appropriate. The rebate period commenced during the third quarter of 2009 and terminates at the end of the fourth quarter of 2010. Customers need to meet certain requirements in order to be eligible for and benefit from this program.

We account for rebates as a reduction to the selling price of our solar modules and therefore as a reduction in revenue. No rebates granted under this program can be claimed in cash and all will be applied to reduce outstanding accounts receivable balances. During the three months ended September 26, 2009 we extended rebates to customers in the amount of €48.7 million ($71.5 million at the balance sheet close rate on September 26, 2009 of $1.47/€1.00) which reduced our accounts receivable from these customers by such amount at September 26, 2009.”

To adjust for this change, our table adds sales rebates back to revenue and adds the rebate reserve back to accounts receivable to arrive at an adjusted DSO figure.

We see that a year after the company extended the payment terms for its customers, the year-over-year growth in DSO stopped. Unfortunately, so did revenue growth which turned negative in 2Q10 despite an increase in DSO. This is a clue that demand had been pulled into the previous quarters and FLSR was unable to stimulate the additional demand necessary to propel growth. First Solar’s stock price soon fell from a late 2010 range of $150-$160 to under $13 by mid-2012.

A More Subtle Example: DENTSPLY SIRONA

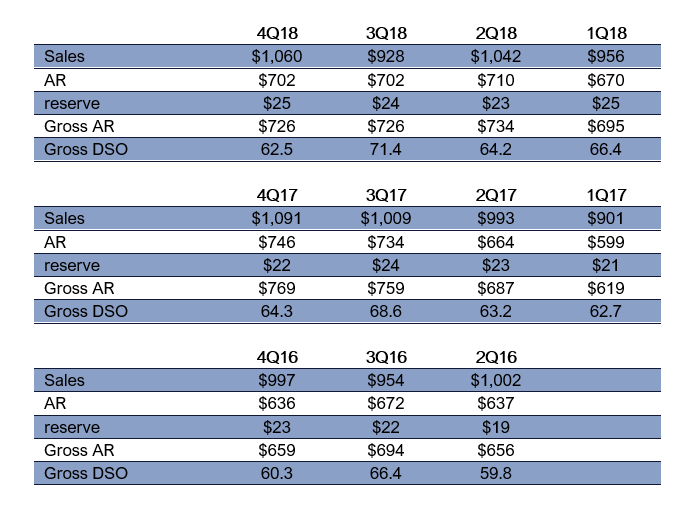

A more subtle example of rising DSOs indicating the pulling of future revenue into the current quarter can be seen in the results of DENTSPLY SIRONA Inc. (XRAY) in the 2018 timeframe. XRAY is a leading manufacturer and distributor of equipment and supplies to the professional dental market. In 2016, Dentsply merged with Sirona to form the present-day version of the company. After the merger was completed, sales growth essentially flatlined for the combined company. The following table shows XRAY’s revenue, accounts receivable, and DSOs for the quarters following the completion of the merger.

However, notice that while sales were practically flat, accounts receivable continued to grow which drove a steady year-over-year increase in DSOs for several quarters. Using a little algebra, we can calculate that if accounts receivable had grown in line with sales, sales would have been 1-5% lower than reported during the 2Q17-2Q18 quarters.

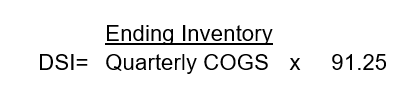

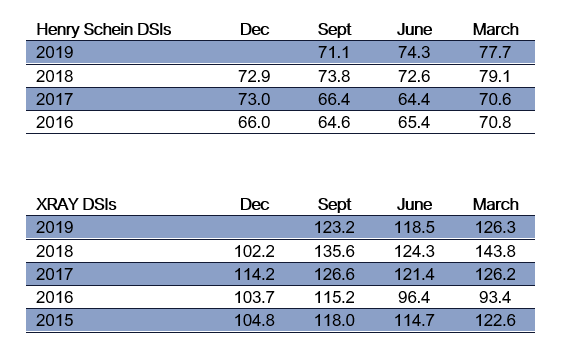

What is especially interesting about the case of XRAY is its two largest customers, Patterson Companies, Inc. (PDCO) and Henry Schein, Inc. (HSIC), together account for about 60% of XRAY’s total sales. They are also publicly traded companies which lets us examine what was going on in their financial statements during the same timeframe as the receivables buildup at XRAY. In this case, we are interested in their inventories. We will examine the analysis of inventories in detail in later articles, but for now, we will quickly introduce the days of sales in inventory, or DSI measure. Similar in concept to DSO, DSI relates the growth in inventory to the growth in the cost of sales and is expressed by the following formula:

The following tables show DSIs for PDCO and HSIC during the periods in question.

The fact that inventory levels at XRAY’s largest customers were rising at the same time its receivables balances were creeping up was pretty strong evidence that XRAY was utilizing more attractive payment terms to entice customers to buy earlier than normal. Unfortunately, the game started to wind down in 3Q18 and 4Q18 when PDCO and HSIC started to pare back their inventories. The following table shows the resulting decline in XRAY’s sales along with an erosion in gross margin caused by pricing pressures.

The weak sales performance resulting from XRAY’s customers working down their excess inventory took its toll on XRAY’s stock price which fell from $66 at the beginning of 2018 to $34 after the third quarter.

The Clues Can Be Subtle

The FLSR example above illustrated an extreme jump in DSOs. The case of XRAY was an example of a more subtle increase in DSOs, but seldom will one have such a clear view into the inventory levels of a company’s customers to confirm the presence of channel stuffing. More often than not, an analyst will not have much to go on to decide if a two or three-day increase in DSOs is something to be worried about or not. This illustrates again how earnings quality analysis is as much of an art as it is a science. A year-over-year increase in DSO of two to three days could be a sign a company is pulling revenue into the current quarter at the expense of the next. Or it could simply be a matter of the timing of collections. To help determine which one, analysts can start by looking in the SEC filings for the quarter or a transcript of the quarterly conference call. Often management may offer an explanation in the liquidity section of the 10-Q or make a comment on the conference call that offers some insight into the increase. However, remember that a great analyst will always take any company explanation with a grain of salt. Any explanation management gives should be tested by asking other questions such as:

What is the company’s recent sales trend? If sales growth has been weakening or barely meeting forecasts for the last few quarters, it should increase the suspicion that the company is using unsustainable tactics to meet the current quarter’s target.

What is the company’s recent history with regards to the quality of reported results? If the company has been slashing discretionary expenses or playing other accounting games with accruals it is more likely that an unexplained or poorly explained increase in DSO is a trick to help the company make the quarter.

What do competitors’ results tell you? It’s not a good sign if a company is posting slightly positive sales growth and rising DSO while its peers are posting sales declines and stable DSOs.

Healthy skepticism and propensity to question what you see can help you avoid unexpected stock price declines like the ones discussed above.

We note that our discussion of FSLR, XRAY, PDCO, and HSIC reflect conditions in the 2010 or 2018-2016 time frame. We currently cover all these companies for our institutional clients, but the discussion above does not reflect our opinion on the current conditions at any of them.

We will examine some of the contra accounts to accounts receivable and how they can be used to manipulate reported results in next week’s Peek Behind the Numbers.

To subscribe to Peek Behind the Numbers for free click here:

If you found this to be helpful, please share with a friend or colleague click here:

Halo! Nice analysis, however I feel to end each section with an example of a decrease in share price is not too appropriate considering that there could be multiple reasons for the price to fall at that time.