The Goodwill Boomerang

The FASB threw out goodwill reform- rising rates may bring it right back again

Last January, we published a report entitled The Impact of Acquisitions on Earnings Quality- Part 1 in which we examined the earnings quality implications of allowing companies not to amortize goodwill. At the time, we were encouraged by the FASB actively considering the possibility of reinstating the amortization requirement. Not long after our publication, the FASB contacted us to get our input on the subject of whether it should again require companies to amortize goodwill or stick with the current impairment model.

Supporters of the impairment model prefer that companies continue to review the fair value of goodwill on an annual basis and record an impairment only when the fair value of the goodwill or intangible asset falls below book value. They contend that a set amortization period is potentially unrealistic as it forces a reduction in the value of an asset that may not have truly depreciated. They also like the simplicity and the fact that IFRS (International Financial Reporting Standards) utilizes the impairment model which increases the comparability of results with the foreign companies they follow.

It should come as no surprise to our regular readers that we argued on the side of a return to amortization. We believe there should be a regular expense recorded to reflect the cost of acquisitions. In fact, last week’s installment of Peek Behind the Numbers discussed how acquisitive tech companies avoid recording a large portion of their true R&D costs by obtaining intellectual property developed by other companies and booking the purchase price as goodwill and intangible assets. The former is not amortized and the amortization of the latter is regularly added back to non-GAAP earnings. You can review that discussion in our last article, Cutting Edge Tech at Absolutely No Cost to You.

There’s no sense in sugar-coating it: we lost. Despite the fact that the FASB had previously seemed to support a return to amortization, it surprised onlookers in June by quietly dropping the matter from its agenda. However, with interest rates rising rapidly, we wonder if headlines reporting a new round of impairments may not bring the matter of goodwill back into focus sooner rather than later.

We will examine the mechanics of goodwill impairment testing and give an example of a company whose goodwill balances may be getting a haircut soon.

Summary of Important Points

It’s not news to anyone that the economy is slowing and profit margins are under pressure – that hurts cash flow.

Also not news to anyone that interest rates are rising – that raises discount rates.

Companies are carrying intangible assets, most notably goodwill, at values that are based on higher cash flow growth and lower discount rates.

Just increasing the discount rates can reduce the value of these intangibles by a significant degree and may produce an avalanche of impairments.

Impairments lower equity/book value and many bank lines have minimum equity levels for companies – renegotiating that clause may boost their cost of capital further,

Impairments highlight failures in past acquisitions and the company’s stock may have had a premium multiple based on it boosting growth with acquisitions and successfully justifying the prices paid – losing that source of growth may cut the company’s P/E or EV/EBITDA multiple based on slower growth.

The Goodwill Impairment Process

When a company makes an acquisition, it determines the fair value of the tangible assets and liabilities of the company it acquired such as inventory, property plant and equipment, accounts payable, and debt. In practice, the purchase price of the acquisitions almost always exceeds the resulting net tangible asset value. This excess purchase price is assigned either to goodwill or intangible assets. Goodwill is not amortized under current accounting guidelines while intangible assets are amortized over an estimated useful life of the asset.

Annual Impairment testing of goodwill

Under current FASB guidelines, companies are required to review the carrying value of their goodwill balances at least annually for indications of impairment. An impairment review can also be triggered by unusual circumstances such as a global pandemic, changes in macroeconomic and market factors, or the reshuffling of segments that requires goodwill to be moved to another reporting unit.

The guidelines for testing goodwill for impairment are spelled out in FASB 350-20-35. The test essentially consists of arriving at a new estimate of the fair value of the goodwill on the company’s balance sheet and compares it to its historical carrying value. If goodwill is being carried on the books at a higher value than the new fair value estimate, an impairment exists.

The Qualitative Assessment

In the interest of efficiency, the FASB allows companies to perform a qualitative assessment before proceeding to the more extensive impairment testing process. At this phase, the company may “assess qualitative factors to determine whether it is more likely than not (that is, a likelihood of more than 50%) that the fair value of a reporting unit is less than its carrying amount, including goodwill.)”

Note that original consideration does not value the goodwill directly, but rather the fair value of the reporting unit which is the value of all assets (including goodwill) less all liabilities. Examples of qualitative factors given include macroeconomic conditions, industry conditions, cost considerations, or declining sales or market share. If nothing in the world, the market, or recent results of the segment in question has changed significantly since the last time the test was performed, the FASB allows the company to rule that it’s simply not worth the effort and expense to have the accountants estimate a value of the segment. However, if management believes there is a greater than 50% chance that the fair value of the reporting unit has fallen below its value on the books, the company must proceed to step one of the process.

Step One

Step one is similar to the qualitative assessment in that the goal is to compare the fair value of the reporting unit to its carrying value, including goodwill. However, step one requires a quantitative valuation of the reporting unit. Guidelines in FASB 350 state:

“The fair value of a reporting unit is the price that would be received to sell the unit as a whole in an orderly transaction between market participants at the measurement date.”

Essentially, the company has been given the assignment of valuing that segment of the business the same way an outside investor looking to buy the business would. This involves all the tools used in your Investing 101 class including discount models, the CAPM, and attaching peer multiples. (We will revisit this in a later section.) The FASB allows for recognizing the value of controlling interest and anticipated synergies yet to be realized. Point of interest: we believe overly optimistic assumptions regarding synergies at the time of acquisition is often the cause of goodwill values unraveling.

If the estimated fair value of the reporting unit exceeds the carrying value of the unit (including the goodwill assigned to that unit) then there is no need to proceed to step 2. However, if it falls below that, an impairment exists and the company must proceed to step 2 to determine its size.

Step 2

So far, the company has been estimating the value of the entire reporting unit supporting the goodwill. Now that it has been determined that an impairment exists, the company must divide that value between net tangible assets and the intangible assets. Consider the following from the FAB guidelines:

from FASB 350-20-35-14:

“The implied fair value of goodwill shall be determined in the same manner as the amount of goodwill recognized in a business combination or an acquisition by a not-for-profit entity was determined. That is, an entity shall assign the fair value of a reporting unit to all of the assets and liabilities of that unit (including an unrecognized intangible assets) as if the reporting unit has been acquired in a business combination or an acquisition by a not-for-profit entity.”

from FASB 350-20-35-16:

“The excess of the fair value of a reporting unit over the amounts assigned to its assets and liabilities is the implied fair value of the goodwill.”

Essentially the company adds up the fair market value of the reporting unit’s assets other than the goodwill being measured and subtracts the market value of all its liabilities to arrive at a net asset value. It then subtracts this from its previous estimate of the fair value for the entire reporting unit to arrive at the fair value of goodwill. The historical goodwill on the books is impaired to the extent that it exceeds the new estimate of fair value. The company must record an impairment expense equal to this amount.

Oh, What a Difference Nine Months Can Make!

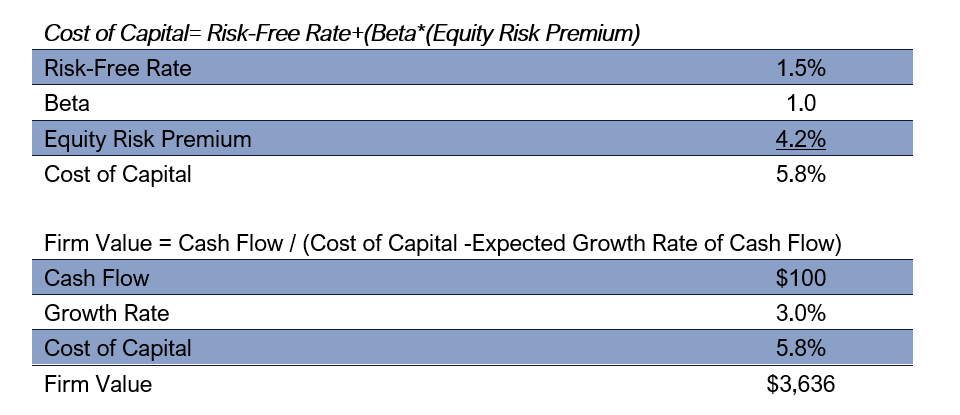

As we saw above, at the heart of the FASB’s process of determining if goodwill or intangibles are impaired is the present value of the future cash flows expected to be generated by the associated segment including all the estimated synergies from combining the operations of the acquired company with the legacy business. A decline in expected revenues or profit margins or a realization that the synergies will not materialize as planned will all drag that value down. However, remember that the discount rate is the input that the present value calculation is most sensitive to. Small changes in that input can yield huge results in the outcome. Let’s value a theoretical reporting unit using a very simple one-stage discounted cash flow model.

We will assume our reporting unit has no debt and will generate $100 in free cash flow in year 1. The cash flow will grow by 3% thereafter. In practice, a company would use very complicated multi-stage models and other inputs. However, for our purposes, the following simple, one-stage cash flow model will suffice:

Firm Value = Cash Flow / (Cost of Capital -Expected Growth Rate of Cash Flow)

Where:

Cost of Capital = Risk-Free Rate + (Beta x Equity Risk Premium)

We will assume the company’s beta is 1.

Let’s calculate our first valuation using market conditions at the beginning of the year. Here, we will borrow from the work of Professor Aswath Damodaran who graciously makes his estimates for US market equity risk premiums available to all. We highly recommend readers check out his latest post, Reaping the Whirlwind, where he presents his estimate for the equity risk premium on 1/1/2022 of 4.2%. Using the 10-year rate on that date, we get the following fair value for the reporting unit on 1/1/2022:

However, let’s recalculate the same fair value using Dr. Damodaran’s current estimate of the US market equity risk premium and the 10-year rate as of 9/23/2022:

Keep in mind, we did not change the assumption in cash flow growth to reflect a slowing economy or an increase in costs. Nor did it include any reduction in expected synergies to be achieved from integrating the unit into the legacy business. However, just the increase in the effective discount rate caused by increases in the risk-free rate and the equity risk premium was enough to shave nearly 60% of our estimate of the fair value of the reporting unit.

Keep this in mind as we move forward.

But Does This All Really Matter in the Real World?

At this point, we are sure some readers are thinking:

“This is all interesting in theory, but don’t impairment charges just get added back non-GAAP adjustments? Besides, isn’t this just a fresh start for the company?”

While it is true that the charges are dismissed by non-GAAP earnings, academic evidence indicates that investors do not completely ignore them and that these companies do pay for this waste of shareholder capital in the form of lower returns. This Journal of Accountancy study from 2012 tracked the relative performance of companies reporting impairments both before and after the initial impairment was reported. A summary of the results is below:

It is not surprising that companies reporting impairments underperform more before the impairment given they have likely already discussed the slowing growth in the segment in question. However, the key point here is that the stocks still underperformed meaningfully in the first six months after the impairment indicating the negative reaction investors had to the news.

A few other studies indicating underperforming stock prices post write-off can be found here:

Li, Z., Shroff, P.K., Venkataraman, R. et al. Causes and consequences of goodwill impairment losses. Rev Account Stud 16, 745–778 (2011)

Bartov, E., Lindahl, F.W. & Ricks, W.E. Stock Price Behavior Around Announcements of Write-Offs. Review of Accounting Studies 3, 327–346 (1998):

Mark Hirschey, Vernon J. Richardson Investor Underreaction to Goodwill Write-Offs. Financial Analysts Journal (2003)

Navigating the Disclosures

The SEC disclosures surrounding company estimates of fair values and the assumptions used to generate them are sparse and vary greatly from company to company. Some companies may give the assumed discount rates and growth rates behind their valuations. Some may even disclose how large a cushion there is between fair values and carrying values. Consider the following disclosure from Church and Dwight’s (CHD) 2021 10-K regarding the value of its trade names. (Note that this addresses the company’s indefinite-lived intangible assets which are assessed in a similar process to goodwill.)

“The Company determined that the carrying value of its trade names as of December 31, 2021 and 2020, was recoverable based upon the forecasted cash flows and profitability of the brands.Fair value for indefinite lived intangible assets was estimated based on a “relief from royalty” or “excess earnings” discounted cash flow method, which contains numerous variables that are subject to change as business conditions change, and therefore could impact fair values in the future. The key assumptions used in determining fair value are sales growth, profitability margins, tax rates, discount rates and royalty rates. The Company determined that the fair value of all indefinite lived intangible assets for each of the years in the three-year period ended December 31, 2021 exceeded their respective carrying values based upon the forecasted cash flows and profitability. The Company’s indefinite lived intangible impairment review is completed in the fourth quarter of each year.

In recent years the Company’s TROJAN® business, specifically the condom category, has not grown and competition has increased. Social distancing requirements due to the COVID-19 pandemic had further negatively impacted the business. As a result, the TROJAN business had experienced stagnant sales and profits resulting in a reduction in expected future cash flows which eroded a portion of the excess between the fair and carrying value of the tradename. This indefinite-lived intangible asset may be susceptible to impairment risk and a continued decline in fair value could trigger a future impairment charge of the TROJAN tradename. The carrying value of the TROJAN tradename is $176.4 and fair value exceeded carrying value by 70% as of December 31, 2021. The key assumptions used in the projections from the Company’s October 1, 2021 impairment analysis include discount rates of 7.0% in the U.S. and 8.5% internationally, growth assumptions based on recent trends, and an average royalty rate of approximately 10%.

While management can and has implemented strategies to address the risk, including lowering our production costs, investing in new product ideas, and developing new creative advertising, significant changes in operating plans or adverse changes in the future could reduce the underlying cash flows used to estimate fair value. In 2021, TROJAN experienced a recovery in sales and profits as it is benefiting from an easing of COVID-19 social restrictions leading to an increase in sexual activity. The Company expects this trend will continue into next year with the continued adoption of vaccines, the reduction of social distancing restrictions and the benefit of management strategies to improve sales and profitability.

The Company’s Passport Food Safety business has experienced sales and profit declines due to decreased demand driven by the COVID-19 pandemic and pressures from new competitive activities resulting from the loss of exclusivity on a key product line. In the fourth quarter of 2021, management’s review of the outlook for the Passport business indicated an assessment of the recoverability of the long-lived assets associated with the business was necessary. That review determined that the estimated future cash flows would not be sufficient to recover the carrying value of the assets resulting in an impairment of the associated tradename and other intangible assets of $11.3. The charge is recorded in selling, general and administrative expenses. The assets have a current remaining net book value of approximately $9.5 and are being amortized over their remaining weighted average life which has been reduced to 7 years. The Company is implementing strategies to address the decline in profitability. However, if unsuccessful, this decline could trigger an additional future impairment charge.”

This disclosure is about as good as you will see. It discloses multiple assumptions about the valuation of the Trojan brand name. It also discloses how large the cushion is between the estimated fair value of the asset and its carrying value. Many times, all that will be disclosed is that the fair value “comfortably exceeds the book value” or “all fair values exceed their book values by at least 20%.”

Proctor & Gamble: An Example of Goodwill Near the Edge

Procter & Gamble (PG) is no longer an acquisitive company. However, deals done decades ago have left the company with a sizeable intangibles portfolio that has incurred multiple, large write-downs. Its Gillette deal has caused it particular trouble. The company has taken huge write-offs related to its shave care including an $8 billion charge in 2019. However, its disclosures indicate we may have not seen the last of the charges.

According to the FY 2022 10-K, annual impairment testing indicated that the fair value of the Shave Care unit exceeded the carrying value by more than 30% while the Gillette indefinite-lived intangible exceeded its carrying value by only 5%. The latter is a very thin cushion. With regards to the outlook for the unit, the company stated in the 10-K that:

“The continued evolution of the pandemic and the Russia-Ukraine War could impact the assumptions utilized in the determination of the estimated fair values of Shave Care reporting unit and the Gillette indefinite-lived intangible asset that are significant enough to trigger an impairment. Net sales and earnings growth rates could be negatively impacted by more prolonged reductions or changes in demand for our shave care products, which may be caused by, among other things: the temporary inability of consumers to purchase our products due to illness, quarantine or other travel restrictions, financial hardship, changes in the use and frequency of grooming products or by shifts in demand away from one or more of our higher priced products to lower priced products or by disruption in the supply chain or operations due to the evolving Russia-Ukraine War. In addition, relative global and country/regional macroeconomic factors including the Russia-Ukraine War could result in additional and prolonged devaluation of other countries’currencies relative to the U.S. dollar. Finally, the discount rate utilized in our valuation model could be impacted by changes in the underlying interest rates and risk premiums included in the determination of the cost of capital. As of June 30, 2022, the carrying values of the Shave Care goodwill and the Gillette indefinite-lived intangible asset were $12.3 billion and $14.1 billion, respectively.”

The company also warned that a continuation of the Russia/Ukraine war could result in a triggering event:

“In light of the Russia-Ukraine War, we performed an additional sensitivity analysis for the Shave Care reporting unit and the Gillette indefinite-lived intangible asset for a range of outcomes, including reduced future cash flows and no future cash flows in Ukraine and Russia. Under these scenarios, the Shave Care reporting unit fair value continued to exceed its carrying value by approximately 30% and the Gillette indefinite-lived intangible asset’s fair value exceeded or approximated its carrying value.

However, if the impact of the war were to extend beyond its current scope, there could be a triggering event for the Gillette indefinite-lived intangible asset that may cause us to perform an additional impairment assessment for that asset in a future period that may result in an impairment charge.”

The company also discloses in the 10-K that a 25 bps increase in the discount rate used in valuing the Gillette name would result in a 6% decline in the value of the asset. This is more than the 5% cushion the company claimed which would seemingly result in an impairment.

Keep in mind that the above were the conditions prevailing on the date that the 10-K was filed in June of this year. Since that time, the 10-year rate has risen from 2.97% to 3.75%, as has any reasonable estimate for the equity risk premium. While the company’s annual impairment test won’t happen again until next June, the current conditions in the market could arguably be considered a “triggering event” for the value of the Shave Care unit to be scrutinized again. With the Gillette asset still carried at $14.1 billion, there seems to be a material risk of another charge.

As we noted above, PG has not been on an acquisition binge in recent years but there are plenty of companies that have. We plan to explore this issue in the weeks ahead and future Peek Behind the Numbers reports will likely discuss other companies that may incur meaningful charges as a result of their upcoming year-end impairment tests.

Contact behindthenumbers@btnresearch.com for questions regarding our institutional research service.

Please share our column with any interested friends and colleagues…

You can follow us on Twitter here

Disclosure:

This article is intended for educational purposes and is not investment advice.

Behind the Numbers, LLC is an independent research firm structured to provide analytical research to the financial community. Behind the Numbers, LLC is not rendering investment advice based on investment portfolios and is not registered as an investment adviser in any jurisdiction. All research is based on fundamental analysis using publicly available information including SEC filed documents, company presentations, annual reports, earnings call transcripts, as well as those of competitors, customers, and suppliers. Other information sources include mass market and industry news resources. These sources are believed to be reliable, but no representation is made that they are accurate or complete, or that errors, if discovered, will be corrected. Behind the Numbers, LLC does not use company sources beyond what they have publicly written or discussed in presentations or media interviews. Behind the Numbers does not use or subscribe to expert networks. All employees are aware of this policy and adhere to it.

The authors of this report have not audited the financial statements of the companies discussed and do not represent that they are serving as independent public accountants with respect to them. They have not audited the statements and therefore do not express an opinion on them. Other CPAs, unaffiliated with Mr. Middleswart, may or may not have audited the financial statements. The authors also have not conducted a thorough "review" of the financial statements as defined by standards established by the AICPA.

This report is not intended, and shall not constitute, and nothing contained herein shall be construed as, an offer to sell or a solicitation of an offer to buy any securities referred to in this report, or a "BUY" or "SELL" recommendation. Rather, this research is intended to identify issues that investors should be aware of for them to assess their own opinion of positive or negative potential.

Behind the Numbers, LLC, its employees, its affiliated entities, and the accounts managed by them may have a position in, and from time-to-time purchase or sell any of the securities mentioned in this report. Initial positions will not be taken by any of the aforementioned parties until after the report is distributed to clients, unless otherwise disclosed. It is possible that a position could be held by Behind the Numbers, LLC, its employees, its affiliated entities, and the accounts managed by them for stocks that are mentioned in an update, or a Peek Behind the Numbers article.