Penumbra (PEN)- Aren't Buybacks Supposed to Be Accretive?

Non-operational benefits and a buyback that doesn't add up

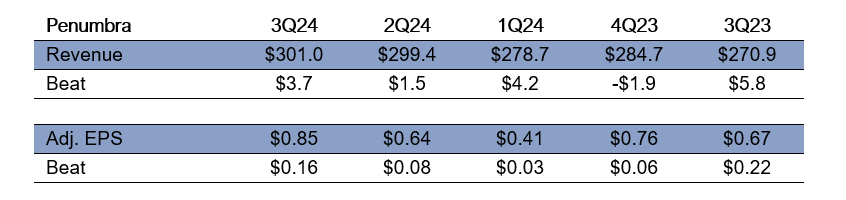

PEN has established itself as a strong growth company in the healthcare products segment, consistently surpassing forecasts for both revenue and non-GAAP EPS. The company beat its revenue forecasts by over 10% in 3Q24, but it slashed its revenue forecast for the full year by $60 million following 2Q24. Here’s a breakdown of the company’s actual results versus expectations over the last several quarters:

While 3Q24 non-GAAP EPS surpassed the estimate by 16 cps, we identified several areas where the company’s recent results have been helped by non-recurring, non-operational items. What’s more, our calculations show that the company’s new share buyback program will likely be dilutive to EPS going forward.

Let’s get behind the numbers…