Dumping the Buyback Kool-Aid

Companies whose buybacks are generating questionable shareholder value

Wall Street’s unquestioning acceptance of the idea that buybacks are always a good use of shareholder capital is one of our pet peeves and a topic we have written about in the past. Last week, while reading our longtime friend Herb Greenberg’s excellent piece on Paycom Software (PAYC), we noticed he pointed out that despite years of sizeable share repurchases, Paycom’s share count hardly ever budges. This got us thinking it was time to do an updated look at the subject.

The basic justification for repurchasing shares often heard in the market is four-fold:

Dividing the value of the company over fewer shares should boost the price of the remaining shares.

Fewer shares outstanding helps boost EPS.

It’s a tax-efficient way to distribute cash to shareholders as there is not a dividend tax.

It should indicate that management believes the stock is cheap.

That last point is very important. Numerous academic studies including Peyer and Vermaelen (2009) and Jagannathan et al. (2000) have pointed to the price at which the repurchases are executed as being a key factor in the value generated by the buyback. Warren Buffett has stated that he prefers a company to repurchase shares when:

“First, a company has ample funds to take care of the operational and liquidity needs of its business; second, its stock is selling at a material discount to the company’s intrinsic business value, conservatively calculated.”

In fact, Harry Singleton, CEO of Teledyne and the father of the buyback, did not regularly buy his company’s shares back but rather opted to make large repurchases when the share price was depressed and the resulting expected return outweighed the expected returns offered by other uses of capital such as reinvestment, dividends, and acquisitions.

Despite this, it has become almost a basic tenant of modern finance that repurchasing shares is an action every company should be doing. Plus, the best time to repurchase stock is always right now! And if a company cannot buy back shares, management will be asked how long before they get their minds right and start. Here are a couple of examples from recent conference calls:

Verizon (VZ) 4Q23 conference call – the company finished recent growth capital spending and is retiring debt:

Analyst – “Tony, can you also remind us when the Board considers share repurchase as it relates to leverage?”

VZ CEO – “Our capital allocation priorities are clear. Number one, money to the business, basically our CapEx. Number two, continue to put the Board in a place where they can continue to increase our dividend. And number three, paying down debt. When we come down to 2.25 times, we have said we will start considering buybacks, but our ultimate long-term goal is to get around 2 times.”

Texas Instruments (TXN) 4Q23 conference call – the company is in the midst of a multi-year expansion program, enduring end-market weakness, and has built up inventory levels all of which consume cash flow:

Analyst – “…obviously that stuff (high capital spending and amassing tax credits) will help the cash flow down the road, but your free cash flow is below the level of the dividend. Right now, I assume it's pretty important to keep paying the dividend. Where does that leave you in terms of share repurchases and other uses of cash?”

TXN CFO – “But big picture understand and look at the operating cash, even in a depressed environment with the revenue, depressed operating cash flow is very strong. We also have very strong balance sheet. And we just finished the year at $8.6 billion. You know, when it comes to repurchases, I would take you to our objectives on capital management for cash return, and our objective is to return all free cash flow via dividends and repurchases. Each one of those has different objectives on dividends and repurchases, but we have a really good track record over many years of doing both of those.”

Let’s take a look at some companies that appear to be doing it right.

LyondellBasell (LYB) – Great Example of How It Should Be Done

LYB is a chemical company with cyclical results, but it normally produces solid cash flow. It can provide investors with long-term growth forecasts because it has cheaper input costs than many competitors around the world. Its goal is always to maintain the current business with capital spending and it wants to pay a dividend. It also evaluates the ROI and valuation of assets based on growing organically with new capital spending, buying other companies, or the accreted value of repurchasing its own stock.

In 2013, LYB started with 576 million shares of common stock. Through June 2023, it repurchased 263 million shares. The share count after that quarter was 324 million. There has been some shares issued to management, but the difference is only 11 million shares. LYB retired 46% of the shares and issued only 2% more.

Its dividend has risen from 90 cents/quarter to $1.25 since 2017. Investors are getting a meaningful and rising yield, but the amount of cash spent on the dividend remains flat over the years at $1.4-$1.5 billion.

It has invested in growth by fixing bottlenecks in the operation over the years, opening new plants, and acquiring others. Baseline EBITDA taking out the highs and lows of the cycles has risen from $6 billion to $9 billion in recent years.

Debt is less than 1x baseline EBITDA and the stock is still cheap to buy with at 4.5-5.0x baseline EBITDA with a yield of 5.2%.

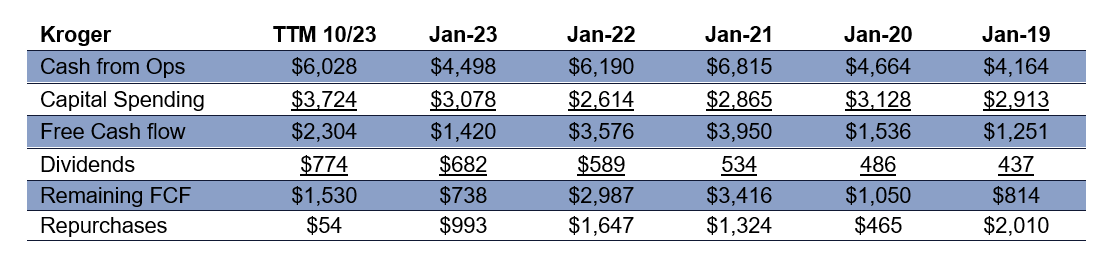

Kroger (KR) Took Advantage of Covid to Buy Shares and Invest in the Business

Since 2027, Kroger bought back 255 million shares and issued 51 million new shares to employees. The drop in share count had been steady but accelerated with the Covid windfall of revenues and cash flow surging during lockdowns.

Rarely did Kroger pay more than 10x EPS for stock. It also ramped up capital spending to help the business and it boosted the dividend too. It wasn’t all stock repurchases. Plus, as cash flow returned to normal levels, Kroger cut back on repurchases and normally spends only about half of free cash flow after dividends on shares.

It has not repurchased shares in the last year. In the 3Q23, the share count actually rose 1 million y/y which was only a 0.1-cent headwind in EPS – a rounding error, and the 96 cents beat by 3 cents. 2Q23 had a flat share count y/y and KR still beat forecasts by 5 cents.

Because KR bought stock back at cheap multiples – it was able to retire 20% of the stock for $6.4 billion. Earnings estimates are for $4.56 in EPS on 725 million shares. Without repurchases, KR would have 952 million shares and EPS lower by $1.09. However, the $6.4 billion at 5% interest income would have offset that by only 27 cents. KR’s repurchase is out-earning the current cost of capital.

However, LYB and KR seem to be the exceptions, not the rule. What concerns us about the market’s perception of buybacks is that so few really look “Behind the Numbers” to see how the repurchases are working out for investors. Very few questions are ever asked – such as:

If a company is buying back shares, why isn’t the share count declining?

Is there cash flow to support the repurchase plan – how is the company paying?

If the company is growing or facing problems – is there a better use for that cash?

Does the company list priorities for using excess cash flow?

Is management overpaying for the shares?

Below we will examine several companies with market capitalizations north of $10 billion that we believe are violating at least one of the above principles.