Costs to Obtain Contracts

The Potential for Accounting for Commissions to Distort Results

Mortimer Duke: Tell him the good part.

Randolph Duke: The good part, William, is that no matter whether our clients make money or lose money, Duke & Duke get the commissions.

-from Trading Places (1983)

In our last installment, we discussed some costs that a company incurs when it makes a sale such as the cost of coupons and rebates that are redeemed later or the liability for potential returns that could occur in the future. Today we will examine the impact of accounting for costs of obtaining a contract and how the company’s assumptions regarding the deal can have a huge impact on the profits the company reports.

Costs to Obtain a Contract- What Is Incremental?

ASC-606 (Accounting Standards Codification topic 606) lays out the framework under which companies recognize revenue and includes the guidelines for accounting for the cost of obtaining a contract. The guideline calls for companies to capitalize the costs associated with obtaining a contract that the company deems to be both recoverable and incremental. Recoverable means that the company expects that it will realize enough revenue under the deal to cover the cost. It is reasonable to expect the typical cost to obtain a contract to be recoverable. However, the determination of whether a cost is incremental can be a little tricker.

The test to determine if a cost is incremental is whether or not the cost would be incurred if the contract was not obtained. A company can spend a great deal of money and effort in getting a deal signed including the cost of travel and hotels, legal work drawing up contracts, and sales commissions. Costs such as travel, the housing and feeding of the sales team, and “wining and dining” the prospect would not be considered incremental as they are incurred whether the deal gets done or not. However, a commission paid to the sales team that is only paid if the prospect signs would be considered incremental. Costs such as amounts paid to a lawyer to draw up a contract that will get paid regardless of the outcome are not incremental, but a fee paid to a lawyer that agreed to only be paid if the contract gets signed would be considered incremental.

Choosing the Amortization Period- Here’s Where It Gets Interesting

Capitalized costs to obtain a contract are to be expensed over the “period of benefit” which is essentially how long the new relationship is expected to generate revenue for the company. If the new client is not expected to renew when the contract expires, then the period of benefit is simply the contract term. However, things are seldom this simple in real life. Customers commonly renew their contract on expiration which requires the seller to estimate the likelihood of renewal and for how many years that will continue. For example, let’s assume a company signs a 3-year contract which results in it paying the salesperson a $12,000 commission. Let’s further assume that none of the commission would have been paid if the contract had not been signed which makes it an incremental expense subject to capitalization.

If the company does not expect the new customer to renew at the end of three years then the company would amortize the $12,000 over the 3-year contract term. However, if the company believes there is a strong likelihood that the client will renew for another 3-year period and then discontinue, then it would utilize a period of benefit of 6 years. (A skeptic will immediately see that a company in this situation might be inclined to assume there will be a renewal to spread the cost over a longer period.)

Salespeople are often paid commissions at the renewal of an existing contract. If the commission rate is the same as the original commission, it is considered “commensurate.” However, these renewal commissions are typically smaller than the original amount and are therefore not deemed to be commensurate. If the renewal commission is considered commensurate to the original, then the company is required to amortize the first commission over the first contract term of 3 years and the second commission over the second three years. If, however, the renewal commission is considered to be not commensurate, the company should amortize the original commission over the full six years of expected benefit and the smaller commission over the final three years.

Considerations and Some Real-Life Examples

Clearly, there is an element of subjectivity involved in accounting for costs to obtain a contract. A company’s policies for accounting for contract costs are typically discussed in the revenue recognition footnote in its financial statements. These policies should be evaluated to see if they line up with what you know about the company’s business model as well as comparing them to the company’s industry peers. Always keep in mind that a company that capitalizes more costs or utilizes a longer period of benefit will report higher earnings than it would if it capitalized less or amortized over a shorter period.

Let’s examine three software companies that utilize very different amortization periods: ANSYS, salesforce.com, and Paycom Software.

ANSYS, Inc. (ANSS)

ANSS provides engineering simulation software solutions. This one is easy to analyze given that it does not capitalize costs to obtain contracts at all. The company stated the following in its most recent 10-K filing.

“We apply a practical expedient to expense sales commissions as incurred when the amortization period would have been one year or less. Sales commissions associated with the initial year of multi-year contracts are expensed as incurred due to their immateriality. Sales commissions associated with multi-year contracts beyond the initial year are subject to an employee service requirement and are expensed as incurred as they are not considered incremental costs to obtain a contract.”

We suspect that the company’s determination that commissions for multi-year contracts are not an incremental cost is a reflection of both how it has structured its sales process and also a desire to simplify its accounting. Either way, the company’s results are not inflated by an aggressive capitalization of contract costs as they are reflected in earnings immediately.

salesforce.com, inc. (CRM)

CRM is a high-profile tech favorite that provides customer relationship management solutions. Unlike ANSS, it has determined that its costs to obtain contracts are incremental and it does capitalize those expenditures. Below are disclosures from its SEC filings regarding its handling of the costs to obtain contracts:

“The Company capitalizes incremental costs of obtaining non-cancelable Cloud Services subscription, ongoing Cloud Services support and license support and updates revenue contracts. For contracts with on-premises software licenses where revenue is recognized upfront when the software is made available to the customer, costs allocable to those licenses are expensed as they are incurred. Capitalized amounts consist primarily of sales commissions paid to the Company’s direct sales force. Capitalized amounts also include (1) amounts paid to employees other than the direct sales force who earn incentive payouts under annual compensation plans that are tied to the value of contracts acquired, (2) commissions paid to employees upon renewals of subscription and support contracts, (3) the associated payroll taxes and fringe benefit costs associated with the payments to the Company’s employees, and (4) to a lesser extent, success fees paid to partners in emerging markets where the Company has a limited presence.

Costs capitalized related to new revenue contracts are amortized on a straight-line basis over four years, which is longer than the typical initial contract period, but reflects the estimated average period of benefit, including expected contract renewals. In arriving at this average period of benefit, the Company evaluated both qualitative and quantitative factors which included the estimated life cycles of its offerings and its customer attrition. Additionally, the Company amortizes capitalized costs for renewals and success fees paid to partners over two years.

The capitalized amounts are recoverable through future revenue streams under all non-cancelable customer contracts. The Company periodically evaluates whether there have been any changes in its business, the market conditions in which it operates or other events which would indicate that its amortization period should be changed or if there are potential indicators of impairment.”

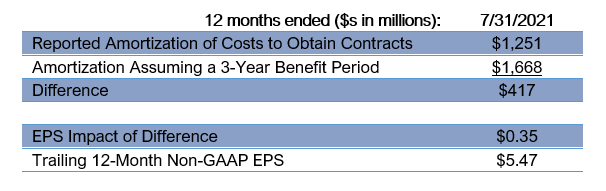

CRM utilizes a 4-year assumed benefit period over which to amortize its capitalized contract costs. The company also boasts of a 90% renewal. This seems to more than support a 4-year assumed benefit period and is in line with its software peers which typically run in the 3-4 year range. Still, let’s take a look at the impact of moving to a 3-year benefit period would have on the company’s earnings:

We see that cutting the benefit period to 3 years from 4 years would cut CRM’s earnings by about 35 cps or around 6% of the reported non-GAAP earnings per share. This is material, but the risk of the company actually having to reduce its amortization period does not seem especially large.

Paycom Software (PAYC)

PAYC provides HR management software as a service (SaaS) solutions for medium and small-sized businesses. Consider the company’s disclosure regarding its accounting for contract acquisition costs from the revenue recognition section of its most recent 10-Q. (Note that PAYC incurs significant costs to fulfill contracts which differ from the costs to obtain a contract which is our focus in this article. Both are discussed in the below disclosure.)

“We recognize an asset for the incremental costs of obtaining a contract with a client if we expect the amortization period to be longer than one year. We also recognize an asset for the costs to fulfill a contract with a client if such costs are specifically identifiable, generate or enhance resources used to satisfy future performance obligations, and are expected to be recovered. We have determined that substantially all costs related to implementation activities are administrative in nature and also meet the capitalization criteria under ASC 340-40. These capitalized costs to fulfill principally relate to upfront direct costs that are expected to be recovered through margin and that enhance our ability to satisfy future performance obligations.

The assets related to both costs to obtain, and costs to fulfill, contracts with clients are accounted for utilizing a portfolio approach, and are capitalized and amortized over the expected period of benefit, which we have determined to be the estimated client relationship of ten years. The expected period of benefit has been determined to be the estimated life of the client relationship primarily because we incur no new costs to obtain, or costs to fulfill, a contract upon renewal of such contract. Additional commission costs may be incurred when an existing client purchases additional applications; however, these commission costs relate solely to the additional applications purchased and are not related to contract renewal. Furthermore, additional fulfillment costs associated with existing clients purchasing additional applications are minimized by our seamless single-database platform. These assets are presented as deferred contract costs in the accompanying consolidated balance sheets. Amortization expense related to costs to obtain and costs to fulfill a contract are included in the “sales and marketing” and “general and administrative” line items in the accompanying consolidated statements of income.”

PAYC states in its 10-K that the contract term for virtually all of its contracts is one month as customers can cancel at any time with just 30 days’ notice. Despite this, we see in the above disclosure that the company utilizes a period of benefit (amortization period) of ten years as it believes it will keep the typical customer that long and therefore the cost of signing them up should be recognized over that length of time. As we discussed with CRM above, most software companies we look at assume benefit periods of closer to 3 years. In other disclosures, PAYC utilizes its 90%+ renewal rate (similar to CRM’s) as a defense for employing such a long benefit period. However, we observe that one of the key selling points for the company is that its solution allows customers to incorporate its solution into its operations very quickly and easily. If it is easy to switch products and competitors such as ADP introduce compelling alternatives, will the company see more customers leaving and have a more difficult time defending its 10-year assumed benefit period? We can’t offer definitive proof that the company will not be able to continue to keep the average customer for ten years. However, the following table demonstrates the impact on the company’s earnings if the benefit period was reduced to 5 years:

We see that cutting the amortization period to 5 years, which is still above most other software companies we see, would cost PAYC almost 50 cps in annual earnings, or more than 10% of annual non-GAAP EPS.

This demonstrates that for some companies, the amortization of costs to obtain contracts can be a significant part of the cost structure, and therefore changes in assumptions can materially impact results. Investors should be aware of this and evaluate any risk that the company might have to change the assumed benefit period in the future.

Note that in addition to costs to obtain contracts, PAYC has significant costs to fulfill contracts which it also capitalizes and amortizes over an assumed benefit period of ten years. We will examine costs to fulfill contracts in a later article.

Other Measures to Monitor for Signs of Increasingly Aggressive Accounting

Companies with material capitalized contract costs typically disclose the balance of the capitalized costs (assets), the amount capitalized during the period, and the amount of amortization. Investors should regularly monitor trends in these two measures to detect any telltale signs of increased aggressiveness:

Amounts Capitalized as a Percentage of Revenue- This measure may vary over time and must be read in conjunction with trends in the overall level of signing new business. For example, software companies typically defer revenue and recognize it over time. Capitalized commission costs for a new deal will all hit the balance sheet at once while the revenue of the deal may be spread out over time. When new business signings are growing rapidly, it may result in an upward trend in the growth of amounts capitalized relative to the growth in reported revenue. However, any increase that cannot be explained could be a warning sign pointing to the company becoming more liberal in what it considers an incremental cost subject to capitalization. This would provide an artificial boost to earnings as more costs are being capitalized rather than expensed as incurred.

·Amortization of Capitalized Contract Costs as a Percentage of the Average Outstanding Balance of Capitalized Contract Costs- this measure should stay fairly steady over time and match the company’s benefit period stated in its footnotes. Any decline in this measure could indicate that the company has started to utilize a longer assumed benefit period. This is particularly important if the company has expressed the benefit period as a range of say 3-5 years.

Please note that the above discussions of PAYC, CRM, and ANSS are not a call to buy or sell or intended to be an assessment of the overall quality of those companies’ earnings.

To subscribe to Peek Behind the Numbers for free:

Please share this article with any of your interested colleagues and friends:

For questions about our institutional research service which provides earnings quality analysis of widely-held names as well as related sell and buy ratings, please e-mail us at behindthenumbers@btnresearch.com.